The split can be anywhere from 50/50 to 90/10 between LPs (aka limited partners/passive investors) and GPs (aka Active partners/Operators/Sponsors). This is applicable for cashflow, refinance and sale equity distribution. The most common split observed is 70% to LPs and 30% to GPs.

Simple Returns through Rental Cashflow

Based on the profit split between GPs and LPs all rental cashflow is shared between LPs and GPs. Similarly, when the property is refinanced or sold, all proceeds are split based on the LP / GP Profit Split.

Preferred Returns through Rental Cashflow

If the deal has a preferred return then, the LPs or passive investors will receive a return of up to X% before the GPs are paid. If the asset cash flows less than X%, the LP receives everything (and their preferred return will accrue for next year). If the asset cash flows more than X%, the LP receive their X% preferred return first and, the remaining profits are again split between the LP and GP. At the sale of the property, after the LP receives the remainder of their equity investment (and if applicable, the accrued preferred return that wasn’t paid out yet), the GPs also receive a catch-up distribution based on the profit split.

Refinance or supplemental loan proceeds:

If the GP refinances into a new loan and/or secures a supplemental loan, the LP will typically receive a distribution that is a portion of their initial equity investment. Similar to the profit split, the proceeds from a refinance or supplemental loan are typically considered a return of capital i.e they reduce the LP’s capital account.

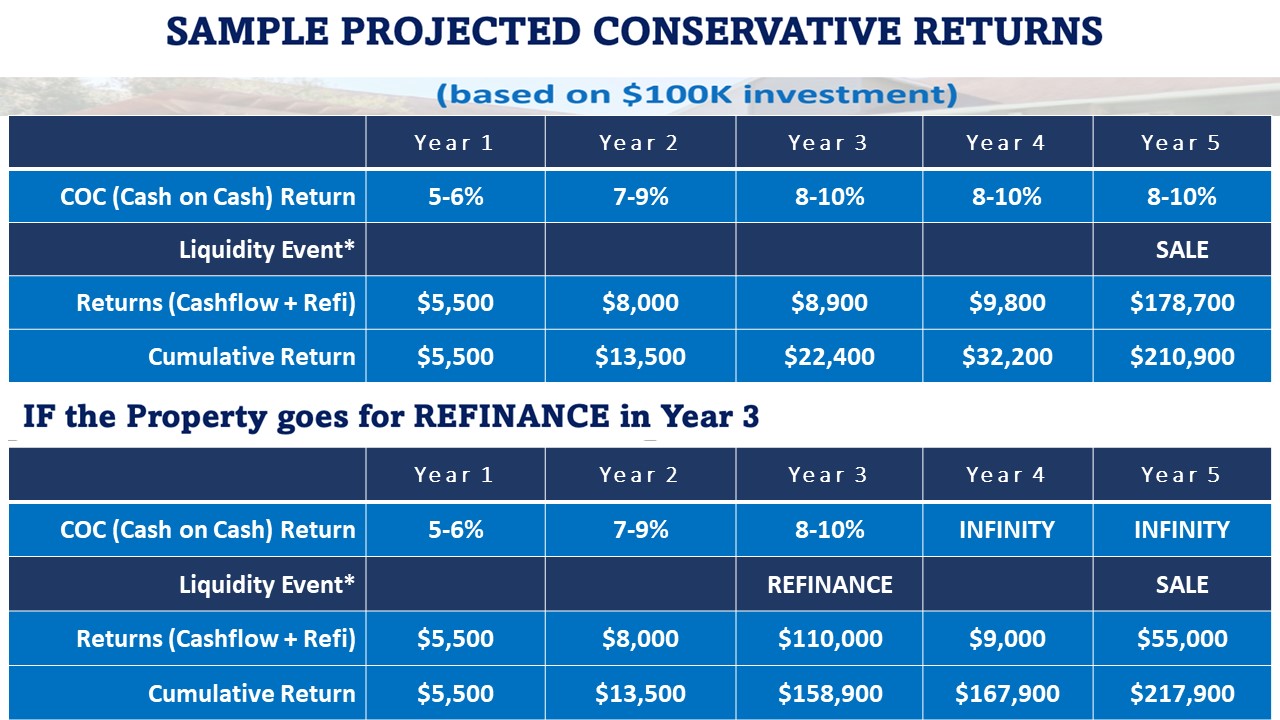

Cash on Cash Return (CoC)

Cash income earned relative to the original cash investment e.g a property generating $10,000 in annual cash flow after debt service and initial cash investment of $100,000, has a 10% cash on cash return. A typical minimum CoC target for syndicated investments is 8-10%. It is not uncommon for the cash-on-cash return to be lower in Yr1-2, while the property is being updated.

Average Annual Return (AAR)

Return on investment averaged over the hold period of the asset, measured as total distribution to members divided by the initial cost of the investment or cash investment. A typical minimum AAR target for syndicated investments is approx. 15%+. It is not uncommon for the average return to be lower in Yr1-2, while the property is being updated and value-add work is ongoing.

Internal Rate of Return (IRR)

This metric captures the full return of the investment including distribution to members (referenced above) coupled with the gain on sale after accounting for time value of money. The timing of when cash flow is returned impacts the IRR. Therefore, the sooner you receive the cash back, i.e. the shorter the hold period, the higher the IRR. A typical minimum IRR target for syndicated investments is 15+ to 20+%.

Equity Multiple (EM)

Measured as total dollars received divided by total dollars invested. Total dollars received includes the cash flow earned throughout the hold period of the asset coupled with the sale proceeds. For example, if you invested $100,000 and you received a total of $200,000 throughout the hold period of the asset including gain on sale, that means you achieved equity multiple of 2.00x or in other words you doubled your initial investment. A typical minimum EM target for syndicated investments is 1.50+ to 2.00+x.

Before

Prospective investors receive an Offering Memorandum which details the property types, markets, and projected returns.

Once you have decided to partner with us, you can register on the investor portal. The link will be sent to you separately.

Investors complete the investment documents and contribute capital.

After

We have monthly investor webinars and, send quarterly investor newsletters outlining the progress of business plan, financials and important updates from the property.

Cash Flow and profit amounts are delivered via wire transfer or ACH to investors linked bank accounts.

You can check live samples of offering memorandum and monthly investor meets HERE .

Cash Flow – Based on your shareholding, the corresponding amount checks are deposited in your account either monthly or quarterly (depending on the distribution process defined for the deal), after all expenses of the property are paid.

Forced Appreciation – Unlike residential, we can force appreciation by value-add strategies in the commercial multifamily property through proven techniques and extensive research of projections before buying.

Tax Benefits – Depreciation is a tax write-off that enables you to keep more of your profits. Passive losses through depreciation are used to write off other passive and capital gains.

Leverage & Amortization – You can get great debt terms up to 60-80% of the property value and paying down debt creates equity leading to long term wealth.

Stability – Multifamily is less volatile and continues to outperform traditional stock-based investments and other asset classes.

Investor Protection –Multifamily syndication offers a secure investment avenue as it operates under SEC regulations, providing transparency, compliance, and investor protection in the dynamic landscape of real estate investments. Leveraging the SEC’s Regulation D, options like 506(b) and 506(c) offerings enhance the credibility and compliance of multifamily syndication, reinforcing a robust and secure investment strategy for our investors.

")

")